Across Nairobi’s sprawling satellite towns—from the dusty plains of Kitengela and Mavoko to the bustling corridors of Ruiru, Juja, and Ngong—a quiet but visible pattern has emerged.

New residential estates launch with glossy brochures, 3D fly-through videos, and ambitious master plans. Yet, five years later, they remain partially completed shells. You drive through them and the anatomy of the stagnation is identical: a grand, completed gatehouse guarding unfinished internal roads; a cluster of beautifully finished model homes backdrop-ing entire blocks of exposed grey concrete and rusting rebar.

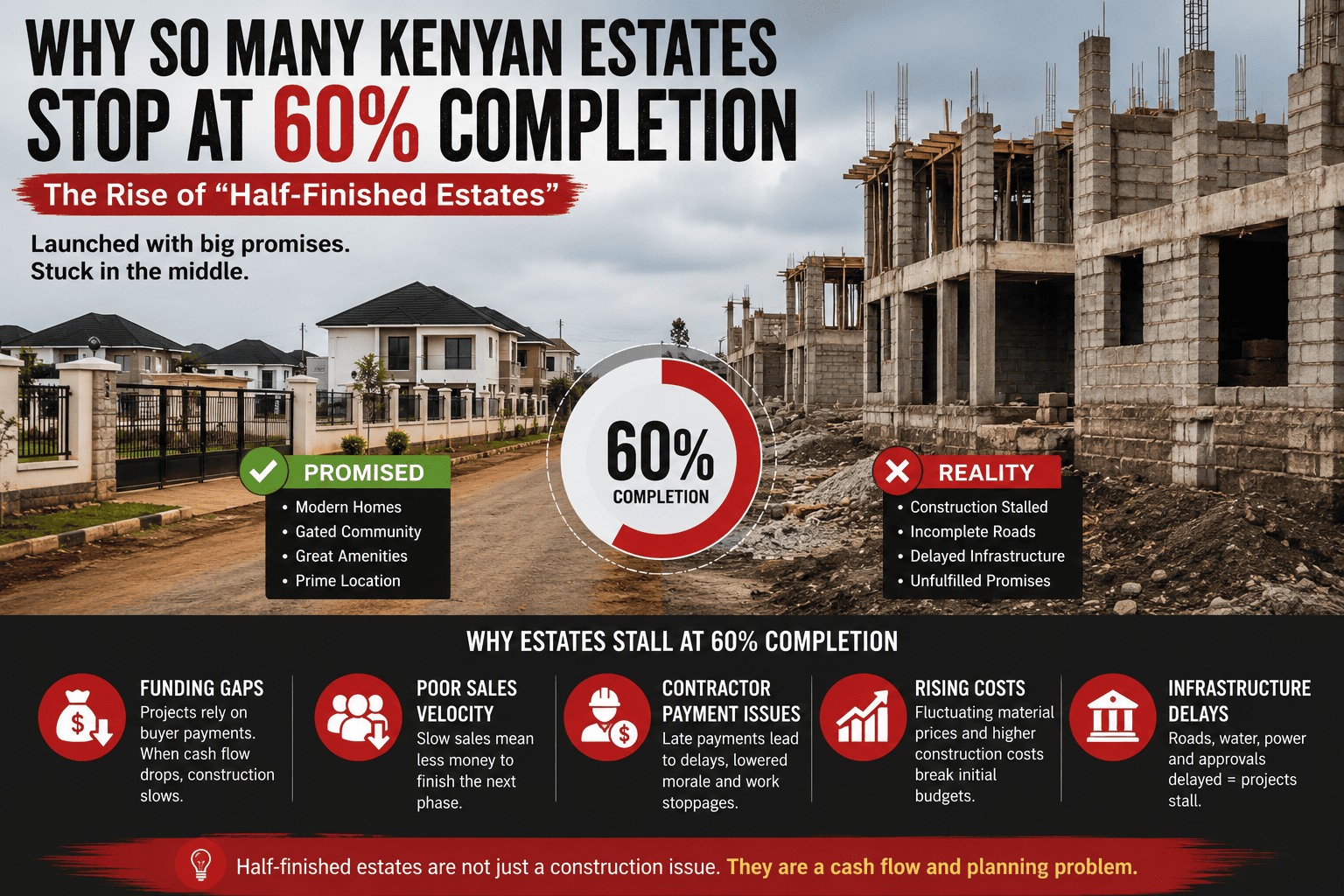

This is not a series of isolated project failures. It is a structural feature of the Kenyan real estate market. Projects rarely collapse in a dramatic wave of bankruptcies; instead, they hit a “60% completion ceiling” and enter a state of permanent postponement.

Here is the sober reality of why Kenya’s satellite estates stop growing, backed by the economic forces shaping the market today.

Read Also:Beyond the Milestone: How the Wealthy Use Real Estate Differently in Kenya

1. The Death of the “Ponzi-Adjacent” Pre-Sales Loop

Most suburban estates in Kenya are built on an fragile self-funding mechanism rather than institutional debt. Developers rely on a highly speculative off-plan model:

Launch Phase 1 (Low Pricing) ➔ Collect Buyer Deposits ➔ Break Ground using Deposits ➔ Sell Phase 2 to Fund Phase 1 Completion

This works beautifully in a roaring economy. But it treats real estate development like a cash-flow conveyor belt. The moment sales velocity drops even by 15–20%, the entire machine grinds to a halt.

Because the developer did not secure full project financing upfront, Phase 1 cannot be completed without Phase 2 sales. When buyers in Phase 2 dry up, Phase 1 construction freezes. The developer isn’t necessarily running away with the money; they are trapped in a broken funding cycle. You aren’t buying a finished house; you are buying into a rolling liquidity pool.

2. The Macro Crises: Hyper-Inflation and Tighter Credit

Developers who budgeted their projects between 2021 and 2023 hit a massive economic wall. Real estate budgets in Kenya have been obliterated by three overlapping macro factors:

- The Sinking Shilling & Import Costs: With the Kenya Shilling experiencing historic volatility against the US Dollar in recent years, the cost of imported finishes, electrical components, and plumbing fixtures skyrocketed.

- The Material Spike: Local construction inputs saw aggressive price hikes. The cost of structural steel and cement rose significantly over the last 24 months, driven by increased manufacturing fuel costs and new tax levies.

- The 18%+ Interest Rate Wall: With the Central Bank of Kenya (CBK) maintaining a high Central Bank Rate (CBR) to fight inflation, commercial bank lending rates soared past 18–20%. Developers cannot afford to bridge their cash-flow gaps with bank loans, and buyers cannot afford mortgages.

When a developer realizes their initial budget is facing a 30% deficit due to inflation, they don’t stop entirely—they slow construction down to a crawl to preserve whatever cash they have left.

3. The Interactive Developer Reality: The “Stall Point”

To understand exactly how tight these margins are, you can look at the relationship between absorption rates (how fast units sell) and construction progress. When sales fall below a critical threshold, a project hits its structural stall point.

The calculator below simulates a typical 100-unit satellite estate development to show how sensitive the “60% ceiling” is to cash flow.

4. The Silent Trigger: Contractor Escrow & Payment Breakdown

When an estate stalls, the developer’s public relations team usually blames “logistical delays” or “regulatory approvals.” The truth is inside the accounts payable ledger.

Construction slows down because of a breakdown in contractor relations. In Kenya, many mid-tier developers pay main contractors in erratic installments tied to sales milestones. When payments lag:

- Subcontractors Mutiny: The main contractor stops paying the specialized subcontractors (electrical, roofing, finishes).

- The Risk Premium Multiplier: Subcontractors walk away. When the developer finally raises cash months later, the original contractors demand a premium to return, or new contractors price the unfinished work significantly higher due to the perceived risk of a stalled site.

This creates a vicious loop: Slow payments ➔ Demobilization ➔ Remobilization costs ➔ Delayed delivery ➔ Buyer lawsuits ➔ Zero further sales.

5. A Hyper-Selective, Cynical Buyer Pool

The Kenyan house hunter has evolved. The era of blind optimism—where buyers blindly cut checks for a piece of red soil and a 3D rendering in Juja Farm—is over.

A wave of high-profile off-plan collapses and land-buying company scandals has made the market deeply cynical. Today’s buyers practice aggressive due diligence:

- They demand to see clean, unencumbered sectional titles before paying substantial deposits.

- They prefer buying near-complete or ready units, even if it means paying a 15–20% premium.

- They carry out independent site visits instead of relying on developer-guided weekend bus tours.

This skepticism creates a catch-22. The developer needs early off-plan cash to build. The buyer refuses to give cash until they see a nearly finished building. Without institutional funding to bridge this trust gap, the project stops moving precisely at the transition from grey shell to liveable estate.

Read Also: What the KNBS 2023/24 Housing and Real Estate Survey Means for Kenyan Home Buyers and Investors

6. Edge-City Infrastructure Misalignment

Finally, there is a physical disconnect between the estate gate and the county infrastructure. Developers often buy cheap, agricultural land deep in the interiors of satellite towns, betting that the local county government will extend tarmac roads, water lines, and electricity grid connections by the time the estate is built.

When the county infrastructure fails to materialize:

- The estate remains inaccessible during the rainy season.

- The cost of hauling water via bowsers or running heavy-duty diesel generators destroys the estate’s viability.

- Prospective tenants refuse to move in, causing buyers who bought for rental yield (buy-to-let) to withhold their final 20–30% completion payments.

The New Normal: Living in a Phased Completion Zone

The result of these forces is the birth of a new urban asset class in Kenya: the Semi-Occupied Phased Community.

These are neighborhoods where life happens amidst perpetual construction. Children play next to stacks of building blocks; early buyers live relatively comfortable lives in Phase 1, looking out their windows at the skeletal remains of Phase 2 and 3.

The 60% completion ceiling is not a failure of brick and mortar. It is the physical manifestation of a broken economic rhythm. In the modern Kenyan market, construction speed is no longer dictated by engineering master plans—it is completely synchronized with erratic, unpredictable micro-cash flows. And until developers move toward institutional joint ventures and project debt over raw pre-sales, our satellite towns will continue to be defined by these half-finished monuments to ambition.